Home purchase or home finances is considered to be the largest investment that a person may ever commit in life. Home loan and mortgage are two charges you will be hearing a great deal when you are buying your first home, refinancing your house and when they take a security of the property using it.

These two terms are likely to be used interchangeably, but these terms are not synonymous. A home loan is normally considered in terms of the global loan product, the money that is borrowed to purchase a home, construct one or upgrade an existing home. Mortgage on the other hand is a legal document or agreement which sets the loan as collateral to the property.

This difference is not purely intellectual in nature – it can have an impact on your eligibility, the rate of interest, the way you repay, taxation and the legal standing that means you can take it as a borrower or owner of property.

The Organisation for Economic Co-operation and Development (OECD) study discovered that in 2024 the global annual household debt was at record high levels with residential mortgages giving over 60% of household lending in the developed world. Equally, the view of the World Bank data indicates that housing finance constitutes more than one-third of credit to households of the entire world thus the significance of comprehending how these devices operate.

This guidebook will give you the sense of understanding on Home Loan vs Mortgage, what they are, their differences, how they operate, and which one would suit you depending on where you are wherever you may be.

What is a Home Loan?

Home loan is one of the financial products where banks, credit unions or other individual lenders provide loans to a person or a family aiming at buying the house as well as construction or remodeling of the house. The borrower is given a lump sum amount, up front, thus indicating that he or she must repay it although he or she will be paying interest on the amount within a definite time frame, in instalments – monthly in most cases.

Key characteristics:

- Purpose-specific: It is mainly used to buy or renovate a house.

- Guaranteed by property: the house per se is frequently a security.

- Long-term tenure: In the majority of markets the term of repayment may be between 10 and 30 years.

- Interest rates: It’s a fixed or variable rate to the business at which it is charged to the borrowing user, according to the market conditions and his credit history.

- Amortized payments: Consistent payments consist of a principal and the interest part.

A home loan will assist you to have a property ownership earlier though in instalment – i.e.- buy and pay as you go over decades. You also need to understand home loan rules and regulations before applying for the loan.

What Is A Mortgage?

Mortgage is not a kind of loan, it is just a legal scheme to secure a loan. You get a home loan with the lender putting a mortgage on the property. This happens to indicate that when you default on repayment duties, the lent party is entitled to own and sell the piece of property in order to get the money back.

Not only are mortgages applied to home loans but also in other credit facilities where property is used as a security or credit which include refinancing, home equity lines of credit (HELOCs), or business loans which use real estate as security.

Core features:

- Security device: Allows the holder of a loan to have a legal title on the property until the loan has been completely paid.

- Collateral: The lender places the lien or charge over the object of ownership which the borrower retains.

- Broad usage: Can secure loans with a wide usage where the loans are not restricted to merely house purchase.

- Legal Registration: It is often registered in the record books of property to give the lender an ownership right over the property.

Summing up the opinions, a home loan is the financial operation, and thus a mortgage is the seizing document which guarantees financial possession.

Home Loan vs Mortgage — The Key Differences

| Aspect | Home Loan | Mortgage |

| Definition | A mortgage to purchase, construct or reconstruct a house. | Security or charge to a loan, which is the legal security of the property to be secured. |

| Purpose | Namely, in residential property purchase or improvement. | Is able to acquire any loan (be it personal, business or home). |

| Nature | Borrowing (financial product). | Legal contract or lien. |

| Collateral | In most cases the house is returning to purchase. | Any real estate which is secured. |

| Ownership | Property is being repaid with the owner living in it. | The borrower is the owner of it, but the lender has a legal claim. |

| Interest rate | Generally lower, aimed at retail customers to the loan facility. | Can be increased in terms of loans secured by building or trading. |

| Tax implications | Some countries may allow deductions in terms of interests and principal repayments. | At any rate; might not receive housing-related tax advantages. |

How Home Loans Work – Step By Step

- Application: You submit an application to a lender providing details on your finances including income, debts, credit score and property details.

- Loan assessment: Your lender will decide and investigate your financial capability in terms of creditworthiness, income-debt ratio, and house value.

- Approval and terms: There is a loan authorization that gives you a loan offer whose terms include interest rate (reward or variable), term or duration, time of payment and other payable interests.

- Disbursement: The lender will issue funds to the seller or the builder or the borrower depending on the purchase or building acquisition progress.

- Repayment: The payment is made in installments (monthly or quarterly) throughout the tenure period until the principal and interest have been paid.

- Mortgage release: When the payment is made in full the lender eliminates the lien against your property by giving you a release or satisfaction document.

Mortgage Structures Around The World

Although the principle itself is the same, i.e. the property provides security to the loan, what happens to be legal and financial-wise most differing across countries are the mortgages:

- United States and Canada: Mortgages are fairly standardized, and are available at fixed rate and adjustable rate. The loans are frequently resold to second markets (e.g. Fannie Mae, Freddie Mac).

- United Kingdom: Mortgages are normally variable-rate mortgages that are administered with stringent affordability criteria.

- Europe: On the one hand, there are numerous countries that provide the flexible category of mortgages and savings are destined to decrease the interest rate.

- Asia-Pacific: There is quite a range in the mortgage-to-GDP ratios; mortgage finance markets are only developing in individual countries.

- Middle East & Africa: There is a very fast increase in mortgages (predominately Islamic based financing the home finance).

Learning the local mortgage systems will assist the borrowers to have an easy time adjusting across regulation, documentation, and foreclosure rights.

Suggested Read: 7-Day Loan Apps

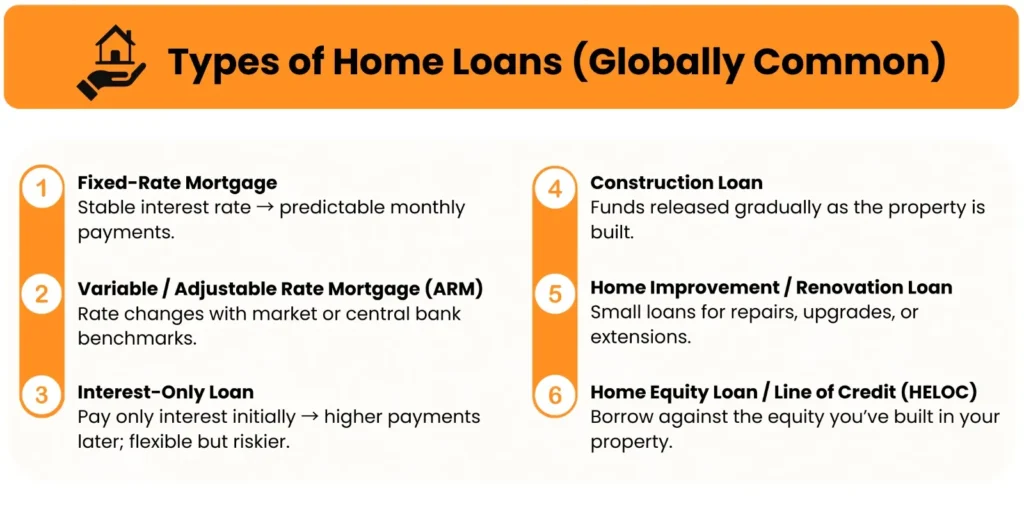

Types Of Home Loans (Globally Common Categories)

- Fixed-rate mortgage- Interest rate stays the same all the way up to the end of the loan period providing predictable installments.

- Variable or adjustable rate mortgage ( ARM )- Interest rate is determined according to the market indices or subsistence levels set by the central bank.

- Interest-only loan- One will only make specific payments such as interest at the very beginning and thereafter higher payments will be made (greater risk but mortgage-like flexibility).

- Construction loan- This is money that is issued as the property can be constructed.

- Home improvement/ reno loan- Minor loans to upgrade, repair, extend.

- Home equity loan / line of credit (HELOC)- Borrow equity that has been accumulated on other costs.

Interest Rates, EMIs, and Repayment – How Costs Add Up

Interest rate, tenure of your loan, and the schedule of repaying your loan are the most serious aspects of your loan.

- Interest rate: It can be either constant or dynamic. Fixed charges are stable; floating charges can be economized in case of decrease in market rates.

- Each payment includes some interest as well as some principal. During early age, the concerns are more on interests; when the person is old the interests pay off to a greater extent.

- Loan term: The more the tenure the lower the payments per month but the higher the overall interest.

- Prepayment: A number of lenders permit early prepayment of the remaining debt – check prepayment penalties.

Example:

The average 300 000 home loan at 5 percent per annum in 25 years will cost you approximately $1 753 monthly. On the full term, you will be repaying some 526,000.00 that is approximately 226000 of interest.

A one-percent percentage difference can save or cost tens of thousands of life time of a mortgage.

Tax Treatment (General Concepts)

Although regulations differ depending on jurisdiction, universal principles have:

- Interest deduction: In a number of countries deductions can be made on mortgage interest payment due on a homestead to a limited extent.

- Capital gain: The sale of your home can lead to capital gains tax, occasionally labored exemptions on in principle homes.

- Proper Taxes: These are usually separate accounts, but can be paid off via a mortgage escrow.

One should never assume that deductions are claimable unless successful verification has been made with local regulations or with a tax advisor.

Choosing Between Home Loan And Mortgage (Strategic Decision)

| Your Goal | Recommended Option | Why |

| Buying a new home | Home loan | Particularly designed in the area of buying property; decreased rates and extended terms |

| Raising funds with the help of current property | Mortgage or home equity loan | Freezes loans not by selling property |

| Debt and financing business. | Mortgage (secured loan) | Loose liquidity; security lowers the risk-level to lenders |

| Better term refinancing of existing loans | Mortgage refinance | Reduces interest rate or alters tenure to be financially efficient |

Common Fees And Hidden Charges

- Processing / origination fee: To assess and to arrange the loan.

- Valuation and legal fees: The assessment of property and title examination.

- Prepayment / foreclosure penalty: Feud over the termination of loans (characteristic of fixed-rate loans).

- Late penalty rates: Service failure to make EMIs on time.

- Conversion fee: Conversion between fixed and variable rate.

These may charge 1-3 percent in addition to your overall rate of borrowing, therefore, read between the lines.

Risks And Responsibilities

- Default risk: Foreclosure and damage to credit-score may come as a result of missed payments.

- Rates edge risk: The variable rates may fluctuate.

- Liquidity risk: Property is not a liquidation and sales may take time to be repaid.

- Legal risk: The risk of not fully documenting your ownership does render it invalid.

- Over-leverage: External borrowing on property may strain your budgets.

Be a responsible borrower- lending companies would give you loans that you will not comfortably repay. Follow the rule of thumb of 30%: your total housing expense (EMI+ insurance + taxes) should not be above 30% of your gross income overtly.

The Application Process (Global Overview)

- Selection of eligibility: credit rating, stability in income, debt split to income ratio.

- Pre-approach: Be aware of the amount that you will be able to borrow prior to house-hunting.

- Compare offers: Compare with lenders Compare among credit unions Compare among fintechs Compare among banks Compare among checked deposit lenders Compare among major official depositors Compare among everyday savings account providers.

- dogging-up paper-work: ID, income documentation, property certificates, valuation statements.

- Underwriting and approval: check all the details will be required before final approval of Lender.

- Conclusion: To sign the mortgage papers, pay fees and the money is disbursed.

- Post closing: Pay the payment on time, amortization, and upkeep of property insurance.

Refinancing And Equity Release

With the changing nature of markets, a significant number of borrowers decide to refinance – take an existing mortgage and a new one at a more favorable rate, or an equally good endowment. Equity release is adopted by other people; under this, you will borrow at a value that you accumulate at your home.

It becomes logical to refinance when the following circumstances are met:

- The interest rate in the market significantly reduces.

- Your credit score improves.

- You have a desire to cut the tenure to save interest.

- You desire to change to a fixed rate whereby you can predict.

Nevertheless, the process of refinancing is not free – make sure that your savings are more than expenses.

The Emotional Side – Beyond Numbers

Homeownership is more than a mere money deal, it is emotional stability, security, and is at times recognition of achievement. But feeling is prejudice to judgment. The issue with numerous individuals is that they overestimate by becoming the ones to spend more money in purchasing a bigger house or underestimate unseen expenses such as insurance, maintenance and property taxes.

The most promising borrowers also take home loans heart first, head first – by buying affordable homes, by having an emergency so that there is always money available and by reviewing financial performance on a yearly basis.

The Future Of Home Financing

The world mortgage market is becoming digital:

- Fintech lenders are presently providing on-request pre-approvals and AI-based risk measurement.

- Smart contracts/blockchain are under experimentation when it comes to property titles and mortgage servicing.

- Green mortgages give incentive to those purchasing energy efficient homes through low rates.

- Shared-equity homes give first-time buyers the chance to share homes with investors or government agencies.

The future looks promising with more transparency and personalisation, and increased convenience delivered by means of digital delivery in the next decade.

Ending Note

It is always necessary to be aware of the difference that exists between home loan and mortgage so that a person is able to make plans to purchase, construct or secure a borrowing facility against the property.

- Living on a home loan is your way to your own house.

- The legal aspects that secure the interest parties are a mortgage and it stipulates what you will do.

Compare International best practices before committing: check on the interest rates, Loan value, repayment flexibility, and the cost of ownership. Always save money, scan all the conditions of the mortgage agreement, and make sure that your long-term finances can afford the unforeseen changes of the rate or even the interruption of the income.

Home financing is not merely a question of the availability of capital, but of order, planning and ownership. The more you are familiar with the operation of these systems, the more intelligent, safe, and convinced is the choice you will make.

FAQs

1. What is the Difference Between Home Loans and Mortgages?

No. A mortgage is the security to a home loan that you have taken.

2. Is it Possible to Take Out a Mortgage as a Reason Other than Purchasing a Home?

Yes. You can use property as security to other loans – business, education or loan consolidation.

3. How Much can I Borrow?

Normally as a percentage of the valuation of the property (usually 70-90%), based on the income and credit history.

4. What Happens if I Can’t Pay?

The lender may foreclose – acquire ownership and dispose of the property in order to recuperate loan amount.

5. Can I Prepay a Home Loan?

Typically yes, though few lenders impose penalties against repayment made prematurely.