The world today mostly depends on mutual funds to accumulate long term wealth among passive investors nowadays due to digitalization. Their use has been driven by accessibility, automation, and transparency, in 2024, amid the beginning of USD 1.4 trillion net inflows into US stock market mutual funds and ETFs alone (Morningstar, 2022), a variant of advancing retail investment.

In the meantime, the total levels of assets under management in the mutual fund business segment, and in asset management in general, keep growing across the globe. Total AUM in the world amounted to USD 128 trillion according to the 2025 asset management outlook by BCG with an increment of approximately 12% annually.

The next major choice arises to the opting retail investor whether to sign up under the Direct vs Regular Mutual Fund plans when investing in mutual funds. Although both these investment options are investing in the same underlying portfolios, these two options have far-reaching implications towards the long-term returns, the control gained by an investor, and the cost-effective nature of the invested amount.

The two approaches discussed in this blog go to the roots of these trips between them, the mechanic of working this or that approach, the differences in cost structure, and looking at how choosing to engage in a specific implementation by differentiating between the two approaches can better suit a particular individual with a financial personality type and goals. This is an important distinction that will have an impact on whether a person becomes a wealthy creation or not, regardless of whether you are experienced or new in the market.

Understanding Mutual Funds: The Foundation

In order to fully realize the distinction between the direct and regular plans, we need to know what a mutual fund is and how it works.

Mutual funds are investment pools of a diversified set of assets which are invested in securities, and are professionally managed by more than one pool of investors. These may encompass either in the form of equities, bonds, money market instruments or a combination of all of the above based on the objective of a fund. The major advantages are diversification, professional management and scale (reduced transaction costs per investor).

In the case of a mutual fund, buying all the units of such a fund is the choice that you make. The Net Asset Value (NAV) is determined on a daily basis: it is the value of the assets less the liabilities of the fund and is divided by the amount of outstanding units. It increases the value of the fund (as a result of good performance of underlying assets) and the NAV also increases and therefore your investment increases.

There are such common types of mutual funds as:

- Growth through stock investments: equity funds.

- Fixed income or debt funds, in the interest of security.

- Balanced or hybrid funds are equity and debt funds.

- Index funds or ETFs are market index funds that track stocks passively.

- Sector or specialty funds which majors on addressing such segments as technology or infrastructure.

Mutual funds enable small investors to access classes and diversification of assets in ways that may be unavailable to them when investing independently due to their ability to pool the funds of investors.

In most areas, mutual funds are also regulated and need periodical disclosure of holdings, fees, performance and audit. Investors are usually redeeming their units at NAV (net of exit load) – that is liquid.

Concisely, the heart of the investment package is composed of obligatory funds; by the direct or the regular schemes, the difference between how much of the performance you retain.

What Are Direct and Regular Plans?

Things may differ regarding the way you invest with a mutual fund despite not changing the fundamentals: it is referred to as direct and regular plans.

Direct Plan

Through a Direct Plan, an investor will be able to invest with the mutual fund provider (AMC, fund house) or through a platform where the fund allows direct investing. It has no intermediary, broker or distributor hence it does not pay commissions or trail fees to third parties. Such setup equals a decreased rate of expenses in comparison to ordinary plans.

In a Direct vs Regular Mutual Fund comparison, the direct plan requires more from the investor—such as selecting funds, tracking performance, and managing redemptions or switches. The merit is that it remains cost-efficient, as every point in fees saved can compound into significant gains over decades.

However, as time has progressed the regulatory changes of most jurisdictions have required fund houses to offer direct plans in addition to regular plans to increase transparency and rights of investors.

Regular Plan

Mutual funds were sold in a traditional way, by a Regular Plan: you invest by a broker, an adviser or a distributor. Such participants aid in fund choice, paperwork, setting up of an account, and follow up services. In these services, the national gets a trail fee or commission, which consequently is part of the expense ratio of the fund.

A fixed plan is, therefore, more costly than a direct one though more convenient with advice and help, which is desirable in case of a naive or less confident investor.

Same Money, Different Streets

It is paramount to point out: direct and regular plans both are invested into the same portfolio and are run by the same portfolio fund manager. It is only a difference in the channel of distribution and the cost layer. Therefore, all deviation of performance is attributed to cost disparities and shareholder conduct- not on the approach underlying these.

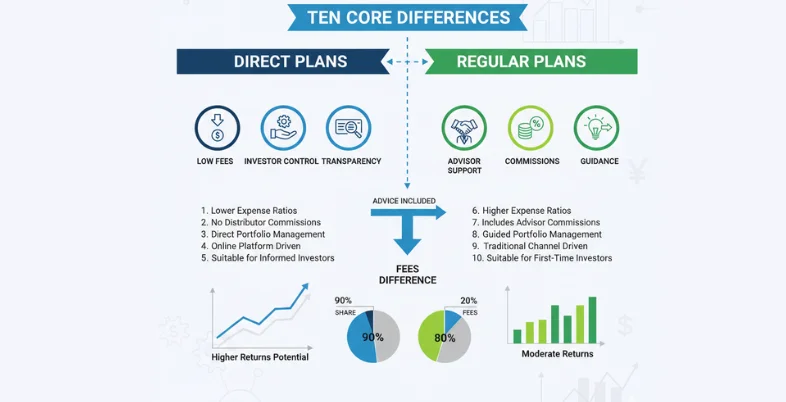

Ten Core Differences Between Direct and Regular Plans

Direct and regular plans differ in ten fundamental ways though the underlying fund is the same and has an influence on the outcomes that appear on the side of the investors.

1. Cost Efficient and Expense Ratio

The only most prominent disparity in a Direct vs Regular Mutual Fund is the cost: regular plans involve distributor commissions in the operating expenses, while direct plans do not. The result is that the cost-to-plan ratio of direct plans is lower. In the long run, even a 0.5–1.0% difference can translate into substantial sums over time.

2. Net Asset Value (NAV)

Direct plans are usually assigned a bit higher NAV as compared to regular plans since a minimal amount is charged against the assets of the fund as fees. As this NAV delta represents savings in cost, it does not always indicate improved portfolio performance.

3. Returns Over Time

Direct plans also tend to outperform regular plans in the long-term under a set of where they have a similar performance and no behavioral setbacks (Hargan, 1982). This trend has been verified through several analysis models around the world (e.g. Morningstar) with respect to equity and balanced funds.

4. Role of Adviser / Distributor

Routine designs consist of advisory support that assists in picking selection, tax planning, and rebalancing as well as in the psychology of the investor, particularly when the stock markets are performing poorly. Direct plans eliminate this middle man making everything the responsibility of the investor.

5. Investor Suitability

Direct plans are well-informed, knowledgeable, self-disciplined investors who like financial savings and exercising control. Periodic strategies are more in line with those who would want to be guided or held by hand, or more new to the investment world.

6. Transparency and Control

In a Direct vs Regular Mutual Fund setup, direct plans are more transparent—the investor deals directly with the fund house, costs are clearly broken down, and they maintain full control over redemptions and switches. In contrast, regular plans may involve intermediary intervention and limited visibility into certain information.

7. Switching and Switching Costs Switching.

Most mutual funds permit conversion of regular to direct plan and vice versa, which is likely to trigger a redemption and repurchase, thus subject to tax or exit load. Plans can be regular plans in which the advisor is transferred; direct plans where the investor makes the transfer.

8. Behavioral Discipline

The routine plans are able to reduce emotional errors through advisor advice – avoiding the tendency to sell rashly when things are not okay. Out of control direct investors have to manage themselves as they mature.

9. Liquidity and Exit Time

Both options bring in liquidity and the only major difference is that regular plans might come with happy exits in the process of making redemptions given the assistance of the advisors. Direct plans can be prone to additional user effort of exit.

10. Access and Barriers

Direct plans need connection to online platforms or AMC interfaces, and they might be not the easiest at first with some investors. Onboarding, paperwork and migration are regularly practiced.

Each of these ten distinctions compound over time such that investment in the first person results in a greater decrease in direct versus regular than the gulf between the two perspectives on wealth and happiness.

Suggested Read: Difference Between SIP and Mutual

Costs, Compounding, and Behavioral Effects

The Effect of Costs with Time

Such a reduced fee might not appear significant in the first place, but in decades such a difference grows exponentially. An equally gross-return fund that has fees 1% lower yields 20-30 percent more after 20-30 years of industry performance. This is the massive grip of cost drag.

Compounding and the “Fee Tax”

In the Direct vs Regular Mutual Fund comparison, fees act as an unchanging tax on your gains. Fund performance may vary, but expenses are always deducted. This is why it’s crucial to choose cost-effective options like direct plans for long-term wealth accumulation.

Psychology of the Stock Market {Investors} & Fallacies

The behavioral error that has been historically observed between the actual and prospective performance of most retail investors involved in investments is that they tend to underperform the funds that they invest in due to behavioral errors. Past scientific studies by firms like Vanguard, Dalbar indicate that the underperformance is a result of poor behavior when faced with performing research. Regular plans conducted by advisors could be a value addition to such investors to keep them in check.

A direct investor has to fight the emotions and follow a plan even during the volatile times, something again not easy without advice.

Technology and Democratization.

The current fintech technologies, such as robo-advisors, goal-based software, fill the gap. They provide online services to participate in fund choice, risk profile, and computer-based investing. Easy access to these platforms has made plan directing more viable to the ordinary investors.

Which Plan Should You Choose?

It does not have a universal best, and the appropriate plan will depend on your style, likes and abilities.

Choose Direct If You Are:

- Knowledgeable on fund, markets and risk.

- Likely doing your research and monitoring.

- Outlined on cost and compounding optimization.

- Confident in remaining disciplined in volatility.

- Choose Regular If You Are:

- Are you an amateur or should you be guided on your portfolio.

- Would prefer to consider fund selection, rebalancing and alignment of the plan.

- Require assistance when going through the roughs.

- Among other things, it will be more convenient.

Hybrid Approach

Most sophisticated investors invest with both simple plans and the satellite plans with conventions through their direct and regular plans, or advisory strategies. That is cost-efficient and expert feedback.

Common Myths Debunked

Myth: Direct gives everything an edge over Regular.

-> Direct lets go a certain-cost off the plate, but ineffective funds ownership may cost even more.

Myth: Charging commissions are the only thing advisors do.

-> Only advisors assume risk absent planning strategy have emotional clarity .A good advisor involves planning, risk management, and clarity of emotion.

Myth: It is difficult to switch.

-> Funds have increased the ease of switching in the majority of markets. Check tax or exit load rules.

Myth: Greater NAV indicates excellent performance.

-> A greater NAV of a direct plan would only result due to reduced costs that do not imply excellent stock selection.

Suggested Read: Home Loan vs Mortgage

Conclusion

The strengths of both plans in a Direct vs Regular Mutual Fund are evident. The direct plan offers cost efficiency, transparency, and control—ideal for informed and disciplined investors. On the other hand, the regular plan provides guidance, organization, and emotional support, making it suitable for new or time-constrained investors.

The right path depends on you. A hybrid strategy is with many success investors. There is an equation of cost control, consistency and emotional discipline with time which are considered more important than the selection of the route which is cheapest.

Be clear: be aware of your style, goals, actions, and ability. Select the plan that you are able to maintain – and leave compounding, barred not by charges, to work in your favor during decades.

FAQs

1. Direct And Regular Plans Which Are Different In Securities?

No Yes, both have the same portfolio run by the same fund manager. The distinction is on distribution and charges.

2. Is It Possible To Switch A Regular Plan To Direct One?

Yes, but it usually comes with redemption and purchase following which taxes or exit loads might be triggered.

3. Is A Higher NAV Always Better?

No, the NAV of a direct plan is better mainly because of reducing fees. There is no difference in the pre fee performance.

4. Which Plan Suits Beginners?

Guide, hand holding, and structured support, not to mention a lowly level of demand, requires regularly planned assistance.

5. Are Direct Plans Necessarily As Cheap?

Yes, in general, but administration, platform or transaction cost might be involved.